Financial Identity as a Service (FiDaaS): A Necessity for Financial Inclusion

Despite Fintech innovations for improved financial services and product delivery, the modus operandi behind the scenes almost remains unchanged. Behind aesthetic user interfaces, banks continue to rely on traditional banking prototypes of branch networks, deficient systems, expensive technology, and a limited talent pool. In addition, they fail to reach and serve the underbanked populations.

Financial Identity as a Service (FiDaaS): A Necessity for Financial Inclusion

The low penetration of the traditional banking system, the rise of mobile phone ownership, and the high proportion of millennials have shifted financial access in a different direction, especially in Africa. Fintech and telecommunication companies collaborate to revolutionize the financial services market and promote financial inclusion through several innovations. These evolutions create a Fintech landscape that overcomes the challenges of the traditional banking system and propels financial inclusion.

Prerequisites for Financial Inclusion

Financial inclusion renders service to the underserved and banks, other financial services providers, and developing economies. Hence, initiatives of the World Bank and United Nations Development Programme (UNDP) place focus on financial inclusion policies. However, achieving financial inclusion requires that certain structures be in place.

The prerequisites of financial inclusion include:

Financial Literacy and IT Education

These are significant tools for financial inclusion. Financial literacy refers to understanding the basic financial concepts required for saving, borrowing, and investment decision-making, as well as market rules, financial products, financial organizations, and regulations. A population’s awareness and perception of financial products and services inclines them towards the financial market and increases financial inclusion. Unfortunately, financially illiterate individuals are often voluntarily excluded from the formal economy and obtain financial information from unreliable sources. Thus, largely resulting in poor financial outcomes.

Moreover, various IT tools have been integrated to deliver more accessible and quality financial services. However, rural and predominantly illiterate populations especially require knowledge and training to use these innovations and build trust.

Internet Access and Innovative Delivery Technologies

Secure internet servers and increased use of the internet promote financial inclusion. Innovative delivery technologies, such as mobile phones, e-money, point of sale transactions, and internet banking, bridge distance and time barriers in access to financial services. Digital banking services are expanding rapidly in developing regions, and the number of active mobile money accounts has increased exponentially.

Regulation

Regulatory frameworks stand as either barriers or pillars to financial inclusion. Therefore, a sustainable financial inclusion policy compels a coordinated regulatory protocol. Regulation of financial services and institutions requires reinforcement to improve credit management, operations, engagement, interest rate, financial reports, crisis, and liquidity risks. Additionally, under regulatory scrutiny, the corporate governance and internal control systems of financial institutions improve to serve customers better.

Data Availability and Financial Identity

Decision-making in the financial industry depends predominantly on data and information. The value and dependability of data that financial institutions have access to affect their service and reputation. Unavailability of accurate data proliferates risk and spurs significant financial losses. Financial Services providers need quality information for risk, operations, valuation, trade, finance, and advanced analytics.

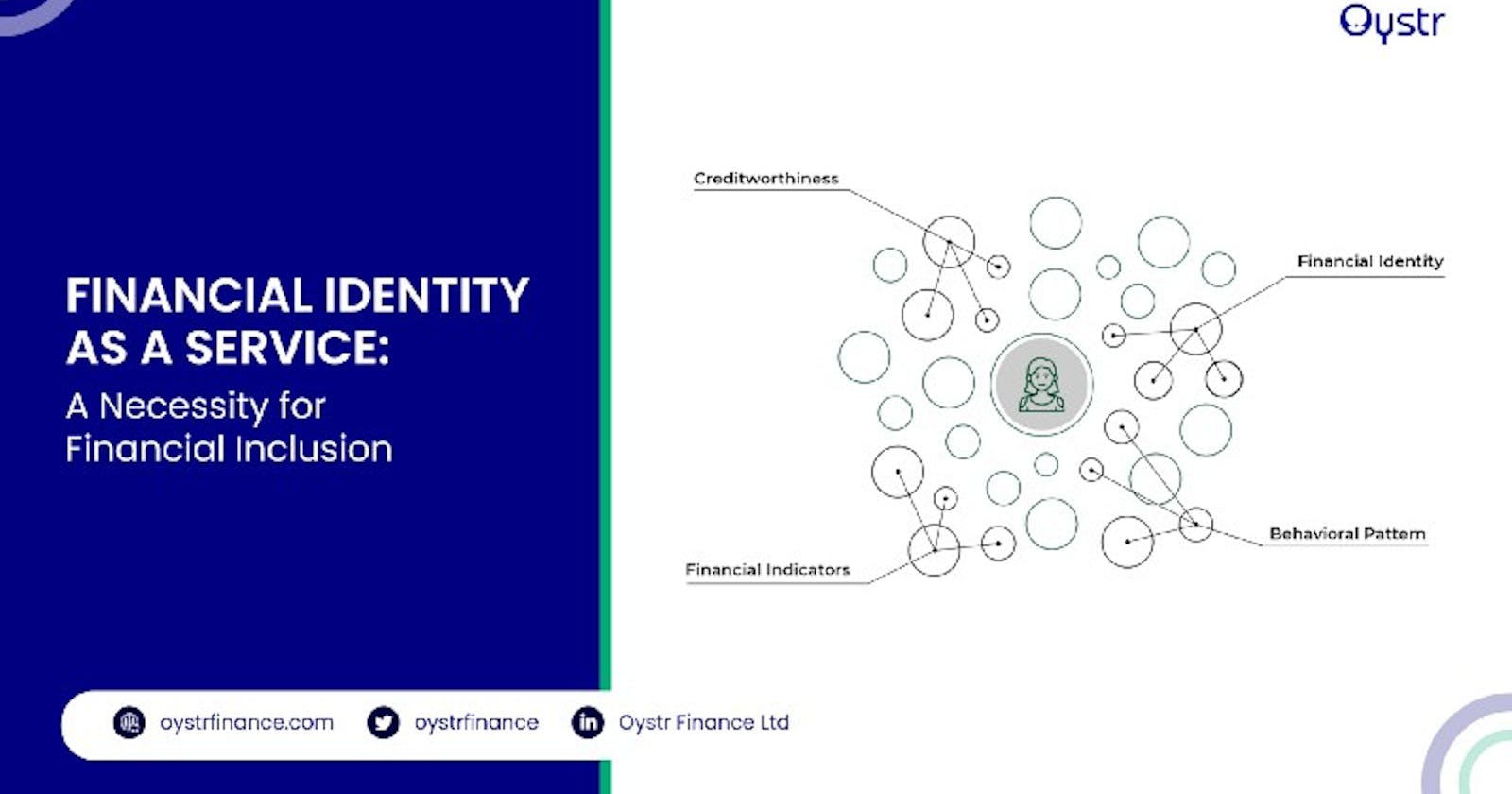

Sustainable data availability remains unachievable without financial Identity. Financial Identity defines a collection of information on the relationship between an individual and money. This could be based on their spending habits, income, or credit habits. Financial identities provide banks and other financial institutions with the information required to prospect and grant customers access to financial services and products. This makes banking relationships less cumbersome and more profitable.

What Is FiDaaS?

Financial Identity as a Service (FiDaaS) is a technology suite built, hosted, and supervised by third-party providers to facilitate creating, using, and distributing financial identities. FiDaaS platforms leverage global cloud infrastructure to consume and present data at scale regardless of time and location barriers. A variety of FiDaaS solutions have been developed to create and provide financial identities for various purposes and users, especially the unbanked.

Most FiDaaS solutions deliver a cloud-based, centralized market data platform. They create standards around data discovery, acquisition, creation, mastering, quality management, and distribution and utilize alternative data.

Hence, the financial identities created and provided by them are reliable, low cost, with high security and zero maintenance.

Why is FiDaaS a Prerequisite for Financial Inclusion?

The financial ecosystem recently experienced a shift towards partnerships between fintech firms and different industries. The merger between traditional banks and telecommunication companies as a major partnership significantly impacted financial inclusion. This consolidation herded the expansion of digital offerings for the underserved in developing markets, especially countries in Africa and Asia.

According to the World Bank, over five billion people globally own and use a mobile phone, while 1.7 billion adults have little or no access to financial services. The World Bank also revealed that one in five financially excluded people blame their unbanked situation on the inability to provide personal information and demonstrate a credit history or account for financial behavior.

Certainly, the amount of documents required for individuals to possess to formulate a financial identity is increasingly confusing. More so, the unbanked and under-banked lack access to the services that provide these identity documents. However, financial institutions require this information to assess new customers. Hence, in the absence of this information, customers exclude themselves before even applying for a financial product or service. Financial Identity as a Service (FiDaaS) makes up for this information deficit by including underserved individuals in the formal economy.

How Does FiDaaS Influence Financial Inclusion?

FiDaaS uses alternative data to create financial identities for the underserved population to ensure their access to financial services. Technological advancement and adoption have given rise to mobile phones’ widespread access and use. As a result, mobile network operators possess large swaths of data on prepaid subscribers, including the unbanked. These data are generated from daily social interactions on mobile phones. This wealth of data includes prospects to create the basis of a financial identity utilized by FiDaaS.

FiDaaS creates a unique financial identity for mobile phone users by leveraging the customer relationships held by mobile operators (MNOs). It models a blueprint for the collaboration of financial service providers and mobile telecommunication operators to promote a more inclusive financial system.

These data can generate insights such as credit scores for mobile phone users. FiDaaS combines mobile phone and broadband access with data science and machine learning. This helps mobile network operators create customer insights such as personal credit scores and provide financial institutions with essential information.

However, the big deal with alternative data includes the size of datasets and the expertise required to extract valuable insights from big data. It requires a modern tech stack to consume high-volume data from different sources and analyze data in real-time.

This is where FiDaaS comes in, that is, the prediction of customer behavior predicted across several transactions, including financial services, by interpreting everyday transactions of prepaid subscribers. FiDaaS helps individuals create financial identities using alternative data and makes them available to financial institutions, telecommunication, and third-party entities. Consequently, the considerable value in emerging markets unravels, and a new generation of customers emerges with the evolving inclusive economy.

Benefits of Using FiDaaS

The merits of using financial Identity as a service cuts across individuals (including the underserved), businesses, financial institutions, regulators, and government. They include:

1. FiDaaS leverages cloud computing to bring digital innovation and delivers financial identities as a service to customers at lower cost, greater security, and no need for maintenance. The use of modern, cloud-based, third-party platforms also ensures high security and data privacy compliance.

2. FiDaaS as a service-based platform ensures the neutrality of data and increases trust in the dataset for the financial institutions to which the data are made available.

3. FiDaaS allows a mobile network operator (MNO) to integrate with multiple banks and enable banks to connect to multiple MNOs simultaneously. It also includes other data partners throughout the digital economy asides MNOs increasingly becoming consumers and contributors to the FiDaaS dataset.

4. FiDaaS platforms deliver financial market data and related services to financial institutions, traders and investors. These primarily include real-time feeds, portfolio analytics, research, pricing, and end-to-end financial data management requirements.

5. FiDaaS improves operational efficiencies by streamlining data management, control, and tracking to enhance governance and verification for regulatory reporting.

6. Financial identities allow targeted, personalized, and prequalified recommendations directly to consumers. This facilitates engagement and repayment of financial services.

7. Providing financial identities for the unbanked and underserved stands at the core of financial inclusion and economic growth. Hence, the use of FiDaaS increases the rate of financial inclusion in an economy.

Final Note

Information gaps challenge the inclusion of the underserved world population in the formal financial system. Financial institutions require a degree of information on a customer’s identity to access services (credit, insurance, savings, etc.). The financially excluded often lack this information and thus, access to these services, further excluding them from the formal economy.

Oystr is using FiDaaS and alternative financial data to provide financial inclusion for the underserved and mitigate risk for financial institutions. Visit our website to learn more.